Willis’s

Elements of

Quantity Surveying

This edition first published 2011

© 2011 Christopher J. Willis, Andrew Willis, William Trench and Sandra Lee

Wiley-Blackwell is an imprint of John Wiley & Sons, formed by the merger of Wiley’s global Scientific, Technical and Medical business with Blackwell Publishing.

Ninth edition published 1998 by Blackwell Science

Tenth edition published 2005 by Blackwell Publishing Ltd

Registered Office

John Wiley & Sons, Ltd, The Atrium, Southern Gate, Chichester, West Sussex, PO19 8SQ, UK

Editorial Offices

9600 Garsington Road, Oxford, OX4 2DQ, UK

The Atrium, Southern Gate, Chichester, West Sussex, PO19 8SQ, UK

2121 State Avenue, Ames, Iowa 50014-8300, USA

For details of our global editorial offices, for customer services and for information about how to apply for permission to reuse the copyright material in this book please see our website at www.wiley.com/wiley-blackwell.

The right of the author to be identified as the author of this work has been asserted in accordance with the UK Copyright, Designs and Patents Act 1988.

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, except as permitted by the UK Copyright, Designs and Patents Act 1988, without the prior permission of the publisher.

Designations used by companies to distinguish their products are often claimed as trademarks. All brand names and product names used in this book are trade names, service marks, trademarks or registered trademarks of their respective owners. The publisher is not associated with any product or vendor mentioned in this book. This publication is designed to provide accurate and authoritative information in regard to the subject matter covered. It is sold on the understanding that the publisher is not engaged in rendering professional services. If professional advice or other expert assistance is required, the services of a competent professional should be sought.

Library of Congress Cataloging-in-Publication Data

Lee, Sandra, MSc, FRICS, MCIOB

Willis’s elements of quantity surveying / Sandra Lee, William Trench, and Andrew Willis. – 11th ed.

p. cm.

Includes bibliographical references and index.

ISBN 978-1-4443-3500-2 (pbk. : alk. paper) 1. Building–Estimates. I. Willis, Andrew. II. Trench, William, F.R.I.C.S. III. Willis, Andrew. Willis’s elements of quantity surveying. IV. Title.

TH435.W685 2011

692′.5–dc22

2011002982

A catalogue record for this book is available from the British Library.

This book is published in the following electronic formats: ePDF 9781444398076; ePub 9781444398083

To the memory of Arthur and Christopher Willis

Contents

Preface

Acknowledgements

Table of Examples

Abbreviations

1 Introduction

2 The Use of the RICS New Rules of Measurement (NRM)

3 Detailed Measurement

4 Setting Down Dimensions

5 Alternative Systems

6 Applied Mensuration

7 General Rules for Taking-off

8 Substructures

9 Walls

10 Floors

11 Roofs

12 Internal Finishes

13 Windows and Doors

14 Reinforced Concrete Structures

15 Structural Steelwork

16 Plumbing

17 Drainage

18 External Works

19 Demolitions, Alterations and Renovations

20 Preliminaries/Preambles

21 Bill Preparation

Appendix Mathematical Formulae and Applied Mensuration

Index

Table of Examples

1 Wall Foundations

2 Basement Foundations

3 Walls and Partitions

4 Brick Projections

5 Timber Upper Floor

6 Traditional Pitched Roof

7 Trussed Rafter Roof

8 Asphalt Covered Flat Roof

9 Internal Finishes

10 Window

11 Internal Door

12 Concrete Frame

13 Structural Steelwork

14 Internal Plumbing

15 Drainage

16 Roads and Paths

17 Spot Items

Abbreviations

a.b. | as before |

a.b.d. | as before described |

agg. | aggregate |

BCIS | Building Cost Information Service |

BS | British Standard |

CAWS | Common Arrangement of Work Sections |

c/c | centres |

ddt | deduct |

diam. | diameter |

d.p.c. | damp proof course |

d.p.m. | damp proof membrane |

EDI | Electronic Data Interchange |

e.w.s. | earth work support |

ex | out of |

hw. | hardwood |

JCT | Joint Contracts Tribunal |

n.t.s. | not to scale |

PC | Prime Cost |

MC | Measurement Code |

n.e. | not exceeding |

NRM | New Rules of Measurement – Order of cost estimating and elemental cost planning |

r.c. | reinforced concrete |

RIBA | Royal Institute of British Architects |

RICS | Royal Institution of Chartered Surveyors |

r.w.p. | rainwater pipe |

SMM | Standard Method of Measurement |

sw. | softwood |

swg | standard wire gauge |

Preface

In recent years the use of the bill of quantities has somewhat declined and today it is only one of a variety of options open to the industry for the procurement of construction contracts. Nevertheless, the skills of measurement are still very much required in some form or other under most procurement routes. The basic structure of the book generally follows that of previous editions, setting down the measurement process from first principles and assuming the reader is coming fresh to the subject. The text has been amended to reflect modern terminology.

Whilst it is recognised that modern computerised measurement techniques utilising standard descriptions might appear far removed from traditional taking-off, it is only by fully grasping such basic principles of measurement that they can be adapted and applied to alternative systems. It is for this reason that the examples continue to be written in traditional form.

This edition recognises the introduction by the Royal Institution of Chartered Surveyors (RICS) of the New Rules of Measurement – Order of cost estimating and elemental cost planning and its relationship with the rules for measurement of building works when producing bills of quantities for tendering purposes.

The book opens with an overview of the need for measurement and the differing rules governing the measurement at different stages of the design or project cycle. The main focus of the book remains on the detailed measurement of elements of a building using the rules from SMM7 and concludes with guidance on how to use the data collected during the measurement process to create the tender documents.

Sandra Lee

William Trench

This book was first published in 1935 and my grandfather Arthur J. Willis, the original author, said in the preface to that first edition that it was intended ‘to be a book giving everything in its simplest form and to assist a student to a good grounding in first principles’. Whilst each successive edition has been brought up to date, we have always striven to maintain the guiding principles he set. In 1968 my father joined my grandfather in joint authorship and on his death in 1983 he took on the work, assisted by Don Newman. William Trench then worked with me on the ninth edition. The guiding principles laid down 70 years ago remain as relevant today as they were then, and have been maintained in this latest edition. Whilst the role of the quantity surveyor is subject to continual change, I am sure that students will find this book as useful as their predecessors have.

Andrew Willis

Acknowledgements

We are indebted to Ruth Pearson, who prepared the drawings. Her efforts are gratefully acknowledged.

Chapter 1

Introduction

The modern quantity surveyor

The training and knowledge of the quantity surveyor have enabled the role of the profession to evolve over time into new areas, and the services provided by the modern quantity surveyor now cover all aspects of procurement, contractual and project cost management. This holds true whether the quantity surveyor works as a consultant or whether employed by a contractor or subcontractor. Whilst the importance of this expanded role cannot be emphasised enough, success in carrying it out stems from the traditional ability of the quantity surveyor to measure and value. It is on the aspect of measurement that this book concentrates.

The need for measurement

There is a need for measurement of a proposed building project at various stages of a project from the feasibility stage through to the final account. This could be in order to establish a budget price, give a pre-tender estimate, provide a contract tender sum or evaluate the amount to be paid to a contractor. There are many construction or project management activities that require some measurement so that appropriate rates can be applied and a price or cost established.

The general approach adopted in this book is to concentrate on the traditional approach to construction whereby the client will employ a designer, and once the design is complete the work is tendered through the use of bills of quantities. Other procurement approaches move the need for detailed measurement to later stages of the project cycle and away from activity undertaken by the client team to that of the contractor’s team.

The need for rules

The need for rules to be followed when undertaking any measurement becomes clear when costs for past projects are analysed and elemental rates or unit rates are calculated and then applied to the quantities for a proposed project. For greater accuracy in pricing it is important to be able to rely consistently on what is included in an element or unit, and this helps build a more reliable cost data base.

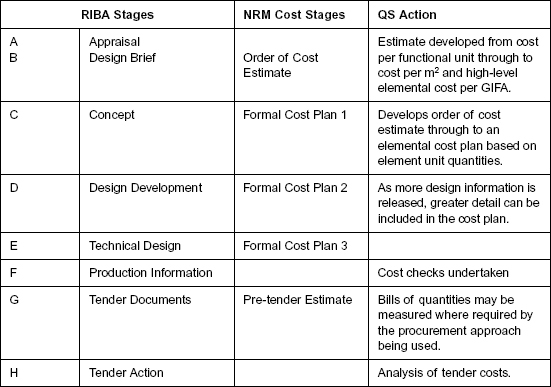

Following the RIBA Work Stages, the measurement undertaken at Stages A and B – Appraisal and Design Brief respectively – the measurement needs to be of basic areas or functional units, and the guidelines of the RICS Code of Measuring Practice are commonly followed. This enables comparisons to be made between different schemes and options when assessing the feasibility of a project.

When preparing a cost plan the need to include the same items in each element is important so that costs for that element can be accurately applied. Few people when preparing a cost plan would refer to the BCIS rules for a standard cost analysis to establish what should be measured with each element. The lack of firm guidelines establishing the ‘standard’ a surveyor should follow led to a variety of approaches being followed for cost planning. In May 2009 the RICS published the first in its planned new set of rules for measurement dealing with order of cost estimates and elemental cost planning. The RIBA work stages and the NRM are explained further in Chapter 2.

The same need for rules applies when measuring for bills of quantities. If a document is to be used for tender purposes and included in a contract then the contractor needs to know the basis of the measurement and what is included or excluded as his price relies on the accuracy of the measure. Historically, standard methods of measurement have been used to provide these rules and are available in various forms world wide.

At post-contract stages it is important that the rules used in the contract document (if applicable) are followed to minimise disputes.

Establishing the approach

The approach to take for any measurement is to decide its purpose and the level of design detail available, enabling the adoption of the most appropriate rules and procedures.

The next chapter will look at the early stages of a building project and the remainder of the book will then focus on the detailed measurement for bills of quantities. Some of the guidance in the following chapters will also enable the appreciation of the rules included in the NRM.

Chapter 2

The Use of the RICS New Rules of Measurement (NRM)

Background

The NRM Project is arguably one of the most significant developments in quantity surveying practice since the publication of the SMM7 in 1988. The intention of the RICS with this publication is to create a set of common rules that provide a consistent approach to measurement through the various stages of a project, from initial cost estimate to detailed quantification of the construction work. Whilst the NRM is based on UK practice, it is nevertheless intended that it should have worldwide application.

This chapter therefore looks at the key features of the NRM in order to explain how it relates to the measurement covered in this text.

Historic industry practice in the preparation of early estimates and cost plans was not to follow any specific measurement rules. Different surveyors would approach the measurement of approximate quantities in different ways: for example, the area of external walls might be measured over windows and doors (i.e. gross measurement) by one surveyor whilst another might deduct the area of the windows and doors (i.e. net measurement). The method of measurement would be closely related to the way in which the rates were to be applied. This variation in practice then resulted in an inconsistent approach to early estimates and cost planning, which then led to further problems where cost plans were used instead of bills of quantities as the basis of tender negotiations. Cost plans would then be analysed and used as benchmarks for further cost plans, thus creating an unreliable data base and potentially inaccurate estimates. The lack of continuity in cost data between cost plans and bills of quantities due to the different basis of measurement means that it is almost impossible to reconcile the cost plan with the pre-tender estimate.

The existing standard for measurement at cost plan stage, which was not official RICS guidance, was the BCIS Standard Form of Cost Analysis (SFCA), which provides a method for capturing, analysing and storing historical cost data. The detail of the SFCA was not always available to those undertaking the measurement or clear to follow. This document was originally developed when bills of quantities were the main method of obtaining a tender price and a substantial data base of project cost information could be established. The cost data was captured in a form that could then be used for early cost advice. The SFCA uses the gross internal floor area (GIFA) as the basis of the cost data, as defined in the 6th Edition of the RICS Valuation Standards (the Red Book) (RICS, 2010). It also promoted the use of element unit quantities and element unit rates for producing cost plans. Although last updated in 2008, some practitioners believe that the SFCA does not adequately address the changes that have taken place in procurement strategies in recent years and the modern day approaches taken in the compilation of cost plans.

The NRM volumes

The RICS plans to publish a suited set of documents in three volumes, for the measurement of building work from the early feasibility stage through to completion, handover and building occupation. The full NRM will comprise:

Volume 1 – Order of Cost Estimating and Elemental Cost Planning, covering:

Volume 2 – Construction Quantities and Works Procurement, covering:

Volume 3 – Maintenance and Operation Cost Planning and Procurement, covering:

Volume 1 was published in 2009. At the time of printing there is no firm date given by the RICS for the publication of MRM Volumes 2 and 3. The RIBA Outline Plan of Work is available from the RIBA website at www.architecture.com, and the UK Government Office of Government Commerce (OGC) Gateway methodology is detailed on their website at www.ogc.gov.uk.

Volume 1 – Order of cost estimating and elemental cost planning

This initial volume provides guidance on the quantification of building works for the purpose of preparing early cost estimates and cost plans. In addition, it gives direction on how to quantify other factors including preliminaries, overheads and profit, project team and design team fees, risk allowances and inflation.

Contents:

For those not familiar with the RIBA works stages, these are included in Table 1.

The structure of an Order of Cost estimate is the same as the Formal Cost Plan 1, thus enabling a consistent approach to be taken as further design details become available. (See Tables 2 and 3.) The rules of measurement, however, differ to take into account the level of design detail available at each stage.

Table 1 RIBA work stages

The different rules for the Order of Cost estimate as opposed to the Elemental Cost Plan can be found by comparing Volume 1 Part 2 with Part 3.

In Part 2 section 2.5 is the measurement rules for building works which give two alternatives depending the level of information available.

Table 2 Structure of the order of cost estimate

| Ref | Items | Currency |

| 1 | Building Works | |

| 2 | Main Contractor Preliminaries | |

| 3 | Main Contractor Overheads and Profit | |

| 4 | Works Cost Estimate Project / Design Team Fees | |

| 5 | Other development / projects costs | |

| 6 | Base Estimate Risk Allowances: Design development risks Construction risks Employer change risks Employer other risks | |

| 7 | Cost Limit (excluding inflation) Inflation: Tender Inflation Construction Inflation | |

| Cost Limit (including inflation) |

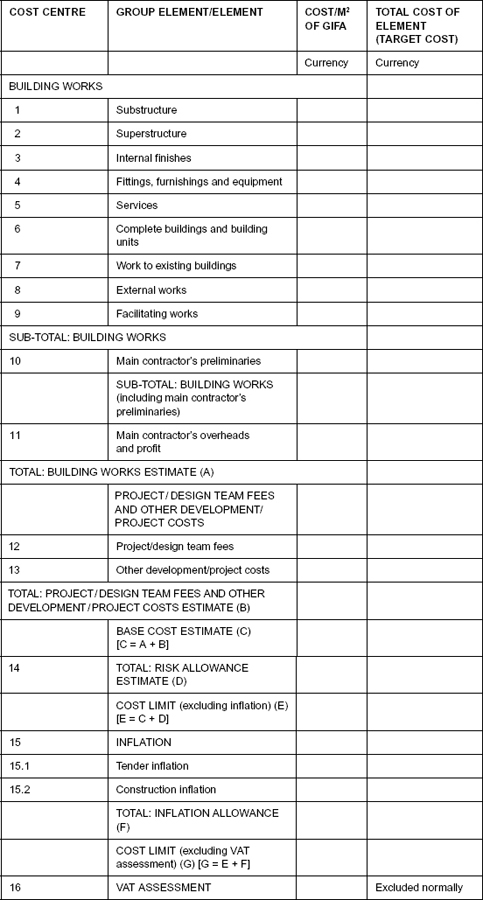

Part 2 section 2.6 gives direction on the use of the Elemental method at this early stage for elements where the information exists. The elements are those listed in Table 3. It is important to note that there can still be optional approaches as the design detail for some elements may not be available. For example, if the external wall details are not available the cost of this element can be found by taking the GIFA × a rate per m2 of the GIFA. If, however, the construction of the walls and windows is known, the cost would be the area of the walls (Element Unit Quantity, EUQ) multiplied by a suitable rate per m2 (Element Unit Rate, EUR) of the walling. The method of measuring and the units are then those contained in Appendix E of Volume 1.

Part 3 section 3.10 contains the Measurement Rules for building works when cost planning. What is a point of note is the statement that the degree of detail of measurement is to be related to the cost significance of the elements in the particular design. Where sufficient information is available, cost significant items are to be measured by approximate quantities rather than the EUQ.

Part 3 has some duplication from Part 2 as there are common areas that need to be included in both Order of Cost Estimates and Elemental Cost Plans. These include everything after the estimate for the building works.

Table 3 Structure of Formal Cost Plan 1

The use of Volume 1 is therefore intended primarily to be restricted to the design stages before production or construction drawings are developed and prior to the preparation of detailed tender documents. There is still a need for the preparation of bills of quantities following the rules of a standard method of measurement where detailed information is provided as the basis for the traditional fixed price lump sum approach to procurement.

A PDF copy of Volume 1 of the NRM is available as a free download from the RICS website to encourage all members to use the guidance. It is a sizeable volume but contains very good instruction on how to prepare early cost estimates and cost plans. It contains useful templates to guide those who do not have them provided by their companies.

An interactive version is also available through the RICS knowledge portal iSurv although this is only available by subscription.

A bound copy of the NRM is available for purchase through RICS Books and other technical bookshops.

The potential benefits of using the NRM

The NRM can be used as a tool for training and education to help develop cost planning skills and is a useful reminder of the items to include. It enables definitive lists of information to be provided to the design team so that they know what needs to be provided for each formal cost plan.

It includes, for defined terms such as building works, estimate and cost limits to provide clearer understanding and consistency. It has also provided a universal work breakdown structure (WBS).

Formal estimating stages have been introduced with clear frameworks to be followed, which should lead to more accurate cost estimates and cost plans. These now consider modern construction products and methods, including modular units and complete buildings and also sustainable construction.

Risk management has been promoted by the inclusion of risk allowances, and the NRM dispenses with the use of the generic term contingency. Inflation has also been considered in more detail with definitions of how to measure inflation and what items to apply this to.

The NRM has been issued as official RICS guidance, and this may create problems for any surveyor who does not follow the guidance should any of his methods be called into question. In the extreme, not following the guidance may also invalidate his Professional Indemnity Insurance.

It is not the intention of this book to be a guide on how to apply the rules contained in the NRM, but merely to make the reader aware of how Volume 1 complements the use of a detailed SMM for the production of bills of quantities.

Little information is currently available about how the rules in Volumes 2 and 3 will be structured, and the SMM7 rules have therefore been used to prepare the measurement examples in this text.